Meet Airlok: The End of One-Sided Verification

As mainstream finance moves on-chain, execution has become instant, programmable, and self-sovereign. Much of today’s crypto stack treats finance as a settlement problem, but real financial markets run on private information about who you are transacting with and what sits behind them.

Today we're unveiling Airlok, Hyve's confidential data layer for finance. A business or originator connects its data into a sealed environment, under rules it sets and can prove Airlok followed. Counterparties query that data directly and get answers back, without ever seeing the data itself. Each answer is live to the source, carries its lineage, and comes with proof of exactly how it was produced. Airlok makes the facts real, live, and queryable, without ever exposing the data. What they mean depends on your question and your risk, so that call stays with you.

Airlok is in beta. We're opening it to partners first and working with them directly on real assets before it's broadly available.

Most verification today is one-sided

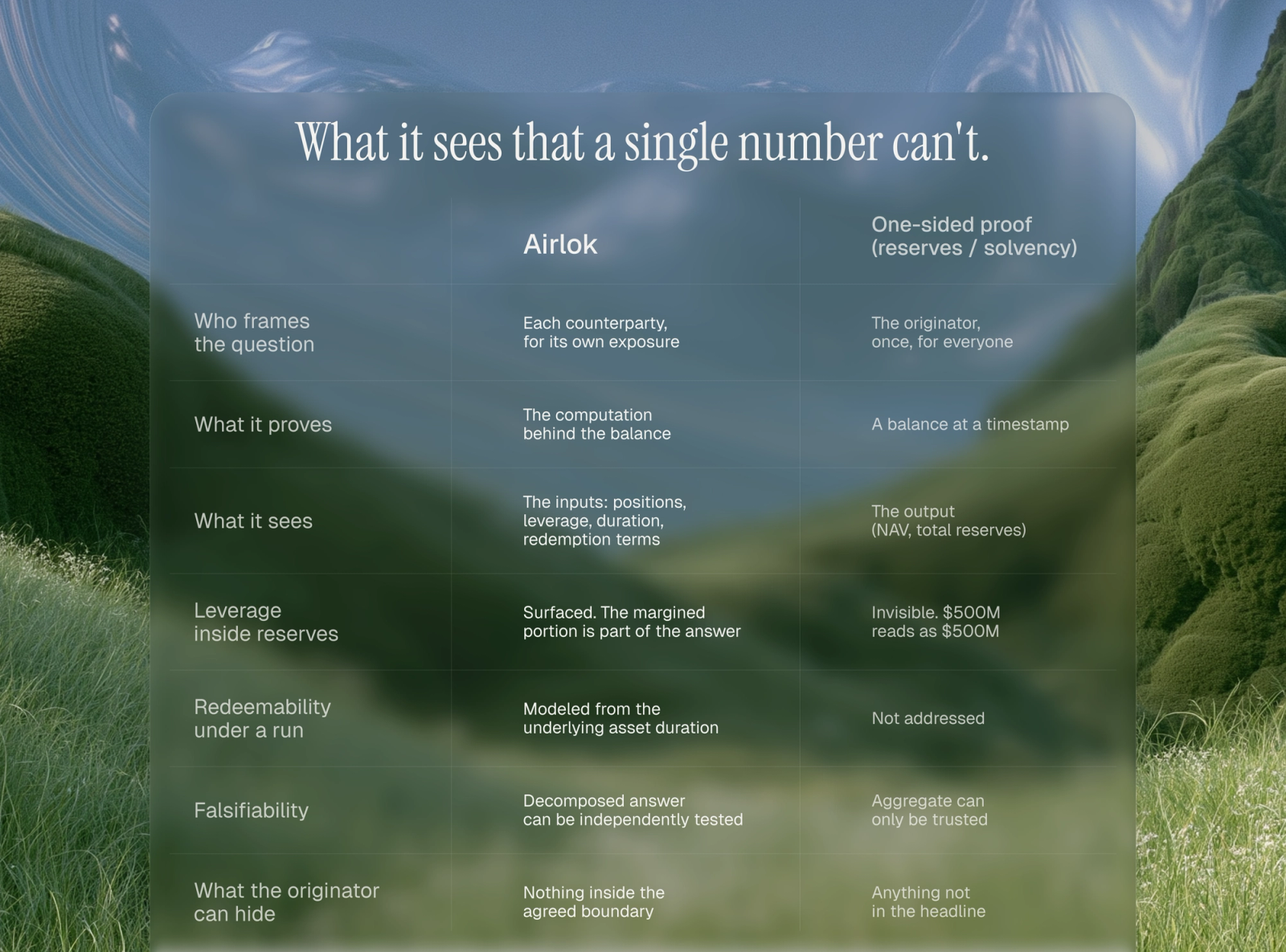

The verification tools on-chain right now are single-sided. Proof of reserves and proof of solvency work the same way: data is pulled from an originator, run through a fixed computation, and published as one number for everyone to consume. The originator decides what gets proven. You consume the result. You can take it or leave it, but you can't interrogate it.

For some assets that's enough. A fully-reserved, liquid, redeemable token doesn't need much more than a credible point-in-time proof that the assets exist.

The problem is that a single published number can only be trusted, not verified. An aggregate with no breakdown is unfalsifiable, there's nothing inside it to test, so you either trust the originator who produced it or you don't. And the originator has no incentive to give you more, because the entire value of a single attested figure, from their side, is that it answers the question without exposing what's underneath. That's not a flaw in any one product. It's what a one-sided proof is built to do: attest a state and stop.

That's the gap the opening described. The attestation was accurate the day it was signed; it just spoke to whether the assets existed, not to the leverage, duration, or margin sitting behind the headline. A one-sided proof attests existence and stops, and existence is rarely the thing that breaks.

Airlok makes verification two-sided

Airlok changes the mechanic by splitting one decision into two.

The party that holds the data sets the boundary of what can be touched. The counterparty decides what questions to ask inside that boundary. That separation is the entire idea, because it pulls apart exposing information from drawing conclusions about it. Two parties step into the same sealed environment instead of one party publishing at the other.

Two properties make the answers worth more than a number an originator would publish on its own:

- The originator can't curate the input. The answer is computed over the full dataset inside the agreed boundary, not the subset the originator would prefer to show. A self-reported figure lets them decide what to hide. This doesn't. They can't bury what's unfavorable.

- The counterparty never sees the raw data. It receives only the answer, computed inside a sealed environment, never the positions behind it. The originator can prove its risk without exposing its book.

So the same underlying facts can answer completely different questions depending on who's asking. Whether reserves survive a run. How a NAV holds up when rates move. Whether there's leverage hidden behind a clean headline. Each counterparty asks in its own way and gets a specific, trustworthy answer, scoped to its exposure, without ever depending on the originator's own reporting.

This is the difference between a published dashboard and a verification you control. One tells you what the originator wanted to show. The other answers the question you actually have, over data they couldn't curate first.\

What it sees that a single number can't

The point isn't that proof of reserves is broken. It answers a solvency question well, and for the right asset it's sufficient. The point is that the products now dominating issuance pose risk questions a single number was never built to reach, and those are the questions Airlok lets you ask.

What you can build with it

The mechanic is general. Here's where it bites first.

Synthetic stablecoins When a lending protocol accepts a synthetic stablecoin as collateral, it's making a credit decision whether it calls it that or not. The risk isn't whether the assets exist. It's what they're made of: leverage that contracts under stress, reserves sitting in margin, redemption terms that can't meet a run. A protocol can use Airlok to verify the leverage and duration that drive its own bad-debt exposure, instead of trusting the issuer's headline.

Duration and risk tranching Products that split senior and junior exposure to the same underlying carry completely different risk under one wrapper. An allocator sizing a position needs the computation behind the NAV: the positions, the leverage ratio, the duration profile, the redemption terms. A vehicle backed by three-month duration assets and one backed by overnight positions can report identical reserves today, and only one can return capital on demand. Airlok surfaces that distinction; the headline number hides it.

Curated vaults A curator publishing exposure to depositors carries the originator's opacity downstream and turns it into its own reputation. Airlok lets a curator decompose and re-prove: take the originator's data as input, verify what it needs proven, and carry a falsifiable answer through to the people relying on it. That's the difference between curating risk and laundering it.

Lending markets broadly Any pool lending against an asset it can't fully see is pricing risk on the originator's word. Airlok lets the pool price it on what's actually true, scoped to the questions its own risk engine needs answered.

In each case the output is the same shape: a signed, fresh, scoped answer that drops straight into a risk engine, an agent's allocation logic, or a settlement contract.

Where this is going

Airlok is the first piece of Hyve we're putting in partners' hands, and it's deliberately the concrete one: a tool you can point at a real asset and get a real answer back. We're starting with partners in beta so we can build it against real exposure, not hypotheticals. The larger story of where two-sided verification leads, once capital is allocated by machines rather than committees, is one our founders will tell separately and soon. For now, the useful version is simple. Money on-chain already moves at machine speed. Airlok is how the truth behind it can move at the same speed, without anyone having to expose their book or take the other side's word for it.

If you're issuing, allocating, or curating on-chain and any of this maps to a problem you have, we'd like to talk. Partner access is open now.

The information in this article is provided for general informational purposes only and does not constitute financial, investment, legal, or tax advice. It reflects Hyve's views as of the date of publication and may change without notice. Hyve makes no warranty as to its accuracy or completeness and accepts no liability for any action taken in reliance on it. Nothing herein is an offer or solicitation to buy or sell any asset or to enter into any transaction.